Faustas Norvaisa

A Growth & Product Expert with 10 years of experience in revenue diversification, international expansion, SEO, and digital marketing. Passionate about scaling businesses and building global brands, he empowers companies to thrive with his motto, "sharing is caring.

Startup funding in Europe in 2026: Grants, VC, angels, crowdfunding, and growth capital

- Last time updated: 20th of May, 2026

Startup funding sources in Europe in 2026 are not limited to venture capital or EU grants alone. Founders can also look at angel investors, crowdfunding, national support schemes, non-dilutive funding, venture debt, accelerators, and growth capital. The harder part is choosing the source that fits the startup’s stage, sector, proof level, and cash need. Many founders waste time applying for money that does not match their business case.

This article intends to explain how European startups can compare funding routes, understand what each source requires, and prepare stronger evidence before they apply, pitch, or raise.

Turn your startup into a profitable enterprise!

Table of Contents

European startup funding is active but fragmented

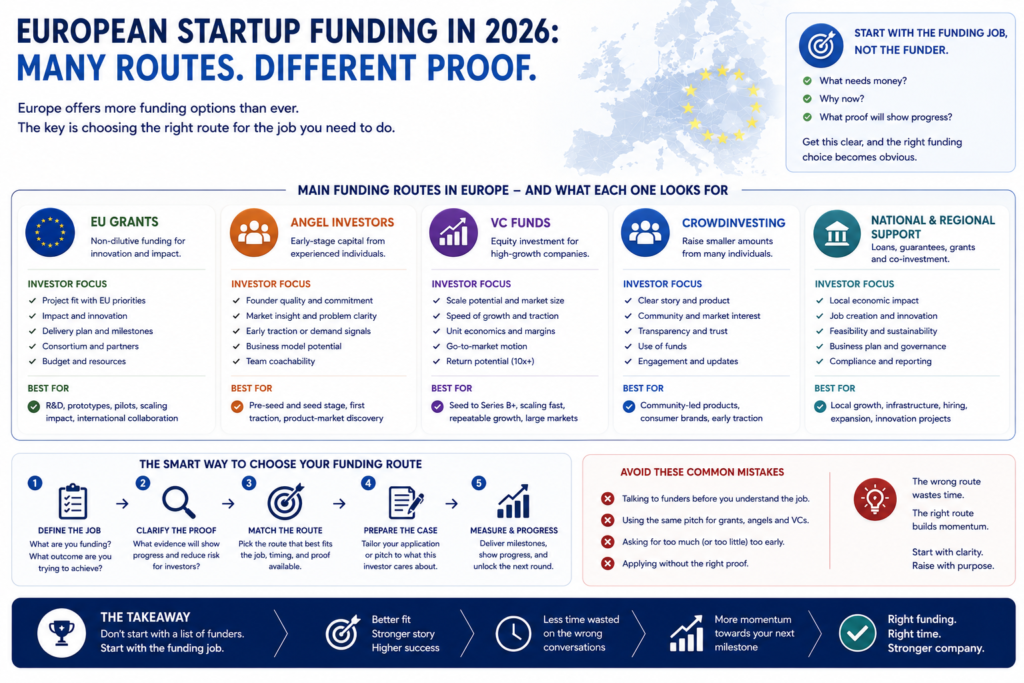

European startup funding in 2026 has many routes for founders, but that choice can create confusion. A company can apply for EU grants, speak with angels, approach VC funds, try crowdfunding, or look for national support.

Each path asks for different proof. A grant will test project fit and delivery ability. An angel will judge founder quality, market sense, and early demand. A VC will look for scale, speed, and return potential. This is why founders should not start with a list of funders. They should start with the funding job: what needs money, why now, and what proof will show progress. Once that is clear, comparing the main sources becomes much easier without wasting time on weak applications or mismatched investor conversations

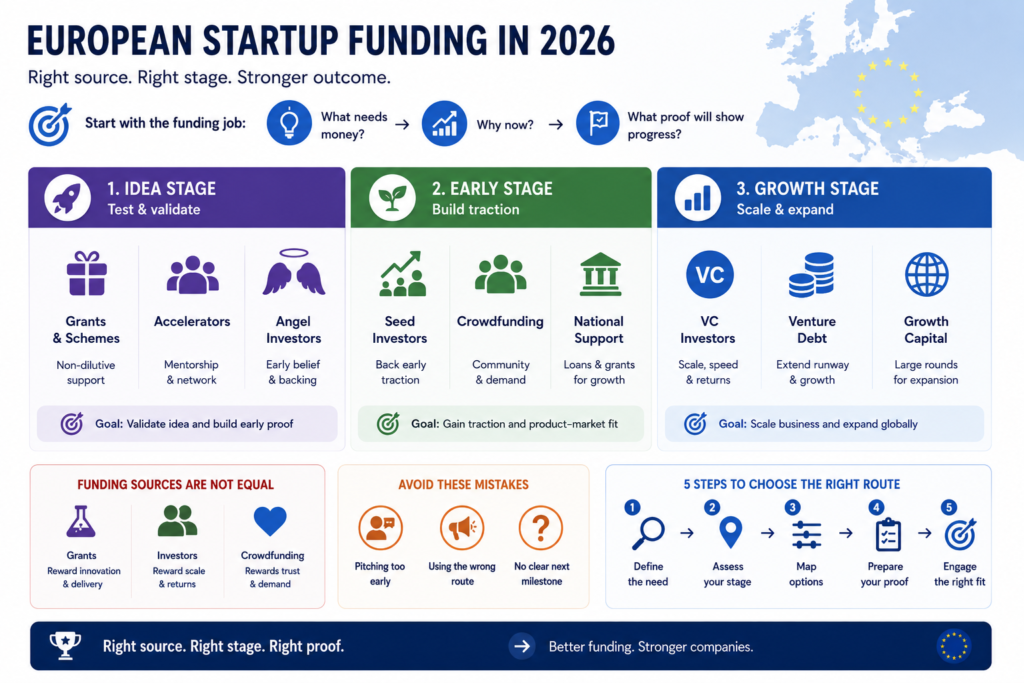

Match startup funding source to Your Current stage

In 2026, European startup funding sources should be matched to the stage of the business before any application or pitch begins. A founder at the idea stage will usually need testing capital, grants, accelerators, or angel support. A startup with early customers can build a stronger case for seed investors, crowdfunding, or national growth schemes. A company with revenue, repeatable sales, and clear expansion plans can look at VC, venture debt, or larger growth capital.

The mistake is treating every source as equal. They are not. Each one rewards a different type of readiness. Non-dilutive funding often rewards innovation and delivery plans. Investors reward scale, traction, and return potential. Crowdfunding rewards audience trust and public demand. That difference matters because the wrong funding route can make a good startup look unprepared.

The main startup funding sources in Europe

Startup funding sources in Europe usually fall into several practical groups, and each one solves a different problem. A founder should know this before building a funding list, because the same company can look strong for one route and weak for another.

- Grants and public programmes support innovation, research, testing, and sector-specific development.

- Angel investors often fit early teams with market insight, founder strength, and first demand signals.

- Venture capital works better when the startup has scale potential, traction, and a large reachable market.

- Crowdfunding can support products with a clear audience, a strong story, and visible community trust.

- Venture debt or growth capital fits later-stage companies with revenue, investors, or predictable cash movement.

This gives founders a more useful way to compare options. The question is not only where funding exists. The better question is which source matches the company’s proof, risk level, and next business step in practice today. It also prevents teams from chasing capital that will never fit their current evidence. After that, non-dilutive funding deserves closer attention because many European founders start there.

Non-dilutive funding in Europe needs clear project fit

Non-dilutive funding in Europe can help startups test, build, or validate without giving away ownership. This route is useful when the company still needs proof before speaking to larger investors. However, founders should not treat grants or public support as easy money. These programmes usually reward clear project fit, measurable outcomes, delivery ability, and strong documentation.

| Funding type | Best fit | What founders should prepare |

|---|---|---|

| EU grants | Innovation-led startups | Project scope, impact, budget, timeline |

| National grants | Local SMEs and founders | Country fit, eligibility, delivery plan |

| R&D programmes | Technical teams | Research logic, partners, commercial use |

| Public loans | Early operators | Cashflow plan, repayment logic, business plan |

This structure matters because non-dilutive funding still has a cost. It takes time, paperwork, reporting, and often strict project rules. A founder who applies without a clear reason can lose weeks on a weak application. A stronger approach is to choose one funding source, connect it to one business need, and prove why the project deserves support now. It also helps founders avoid mixing unrelated goals, such as product testing, hiring, market entry, and research, into one unclear request.

For many European startups, this can create the evidence needed before angels, VC funds, or growth investors enter the conversation. Once that base is ready, investor-led funding becomes easier to compare against the startup’s next real commercial milestone.

Investor-led funding in Europe depends on scale proof

Investor-led funding in Europe should be used when the startup can show a path toward meaningful growth, not only a need for cash. Angel investors can support early teams when the founder has strong market insight, first customer signals, and a clear next milestone. Venture capital needs a sharper case. VC funds usually look for large markets, faster growth potential, strong margins, and a team that can scale across countries or sectors.

This matters because investors are buying future upside. They will ask whether the startup can grow beyond local demand, founder-led sales, or one early customer group. A strong pitch should connect traction, pricing, customer acquisition, product delivery, and use of funds into one clear story. Without that link, the raise can look premature. Next, crowdfunding deserves attention because it can turn public demand into capital before larger investors join.

Crowdfunding in Europe can turn demand into funding

Crowdfunding in Europe can work well when a startup has a clear audience, a strong reason to believe, and a product people can understand quickly. It is not only a way to collect money. It is also a public test of trust. MarketDataForecast estimated the Europe crowdfunding market at USD 9.95 billion in 2026, up from USD 8.44 billion in 2025, which shows that this route is becoming a more serious part of the startup funding mix.

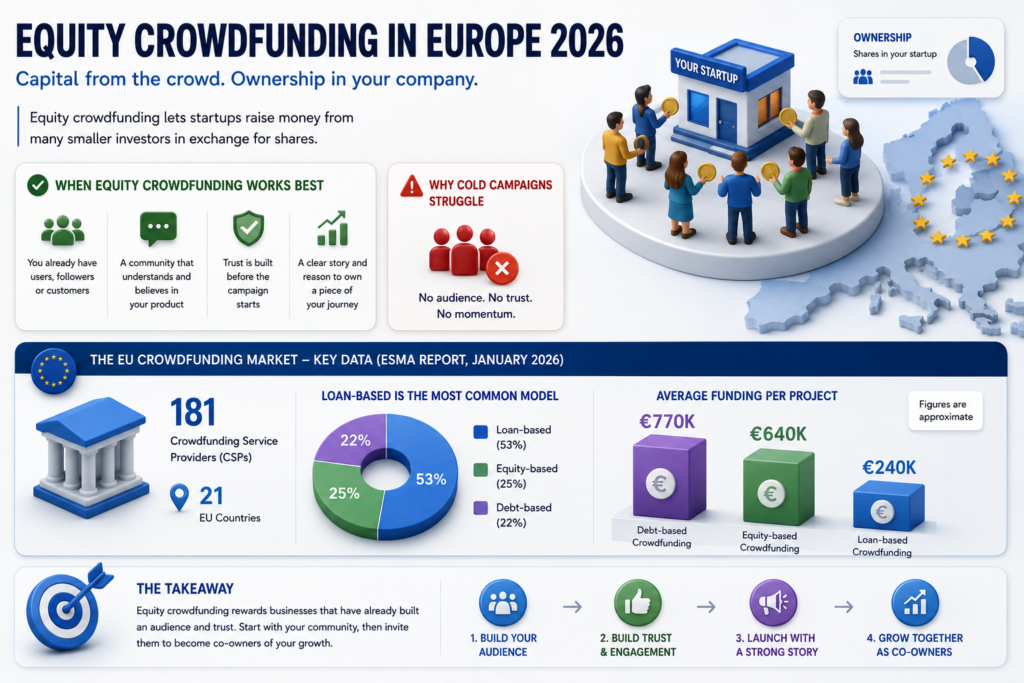

Equity crowdfunding fits community-backed startups

Equity crowdfunding can help startups raise money from many smaller investors in exchange for shares. This route often works better when the company already has users, followers, customers, or a community that understands the product. A cold campaign with no audience usually struggles because trust has not been built yet.

The EU crowdfunding market also shows why founders need to choose the right model. ESMA’s January 2026 market report showed 181 crowdfunding service providers across 21 countries, with loan-based funding as the most common model. It also reported that average funding per project was about €770,000 for debt-based crowdfunding, €640,000 for equity-based crowdfunding, and €240,000 for loan-based crowdfunding.

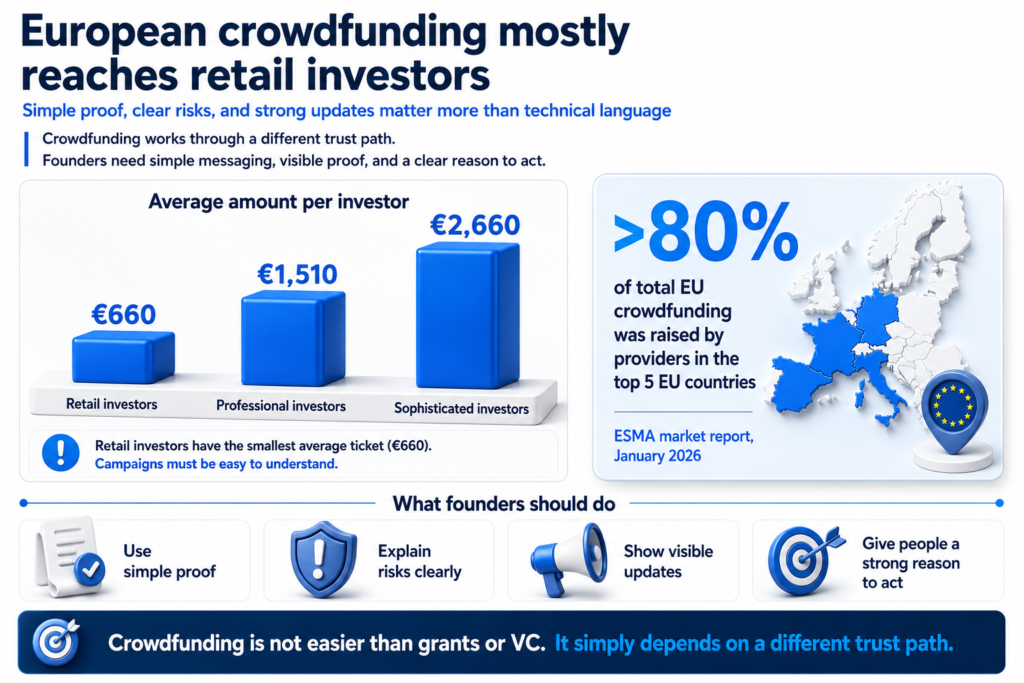

Retail investors change the trust equation

European crowdfunding mostly reaches retail investors, so the campaign must be easy to understand. ESMA reported that the average amount per investor was around €660 for retail investors, compared with €2,660 for sophisticated investors and €1,510 for professional investors. That means founders cannot rely on technical language alone. They need simple proof, clear risks, visible updates, and a strong reason for people to act.

Crowdfunding still needs serious preparation

Crowdfunding should not be treated as easier than grants or VC. It simply uses a different trust path. ESMA also found that providers in the top five EU countries raised over 80% of total crowdfunding across the EU, which shows that location, platform choice, and investor access still matter.

Founders should prepare campaign pages, product visuals, financial notes, founder videos, delivery timelines, FAQs, and risk explanations before asking for money. When used well, crowdfunding can support both capital and credibility. From there, later-stage companies should decide whether venture debt or growth capital fits their next milestone.

Venture debt, VC, and growth capital show where Europe is moving in 2026

Venture debt, VC, and growth capital in Europe in 2026 are not moving in one simple direction. The market has money, but that money is becoming more selective, larger in ticket size, and more focused on companies with proof. Founders should read this as a signal. If the startup is still proving basic demand, grants, angels, or accelerators might fit better. If the company has revenue, technical strength, strong investors, or a clear expansion case, then venture debt, VC, or growth capital can become realistic.

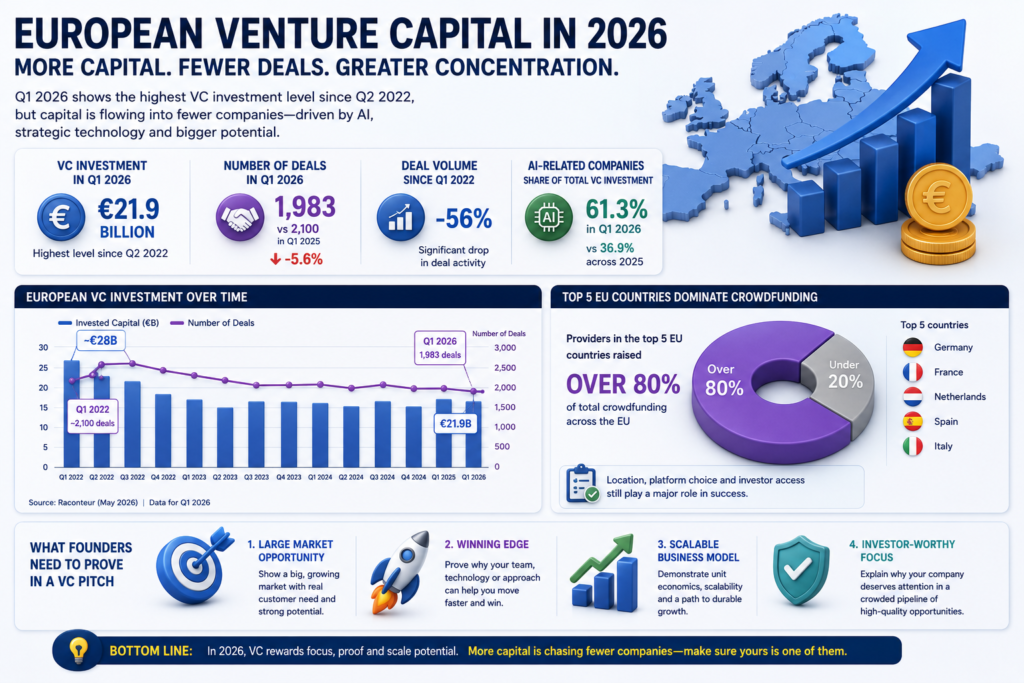

VC value is rising while deal volume is falling

European venture capital in 2026 shows a clear concentration trend. Raconteur reported that European businesses attracted €21.9 billion in VC deals in Q1 2026, the highest level since Q2 2022. However, the number of deals fell from about 2,100 to 1,983 in the same quarter, while deal volume has dropped 56% since Q1 2022. AI-related companies also took 61.3% of total European VC investment in Q1 2026, up from 36.9% across 2025. That data proves the point better than any general statement: more capital is going into fewer companies, especially where investors see AI exposure, strategic technology, or larger upside.

For founders, this means a VC pitch needs more than ambition. It should prove why the company can win a large enough market, why the team can move faster than competitors, and why the business deserves investor attention in a crowded pipeline.

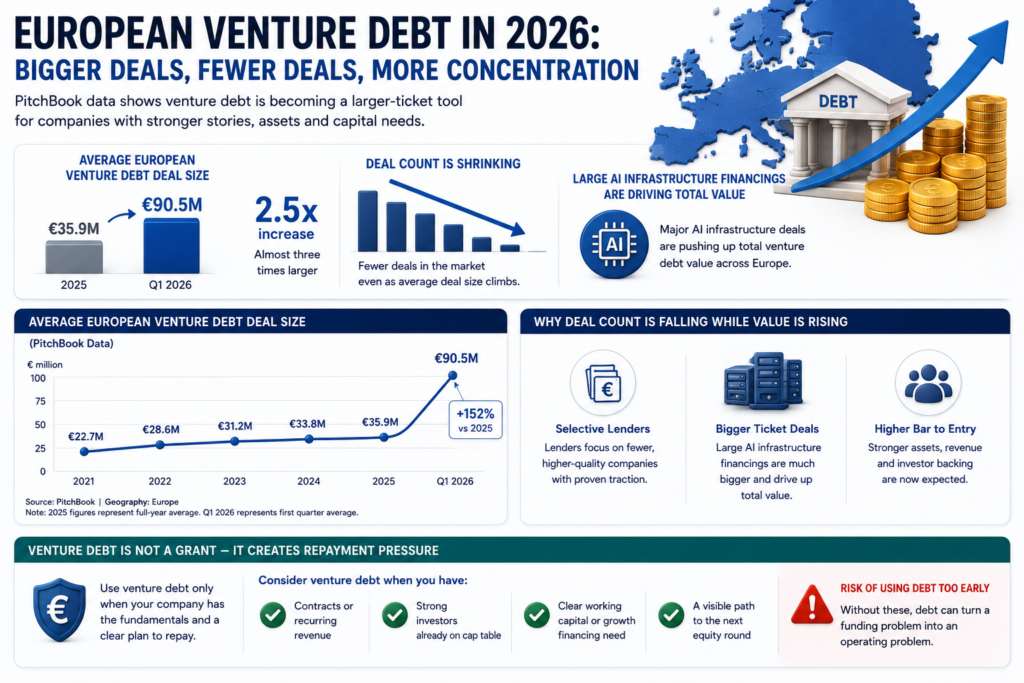

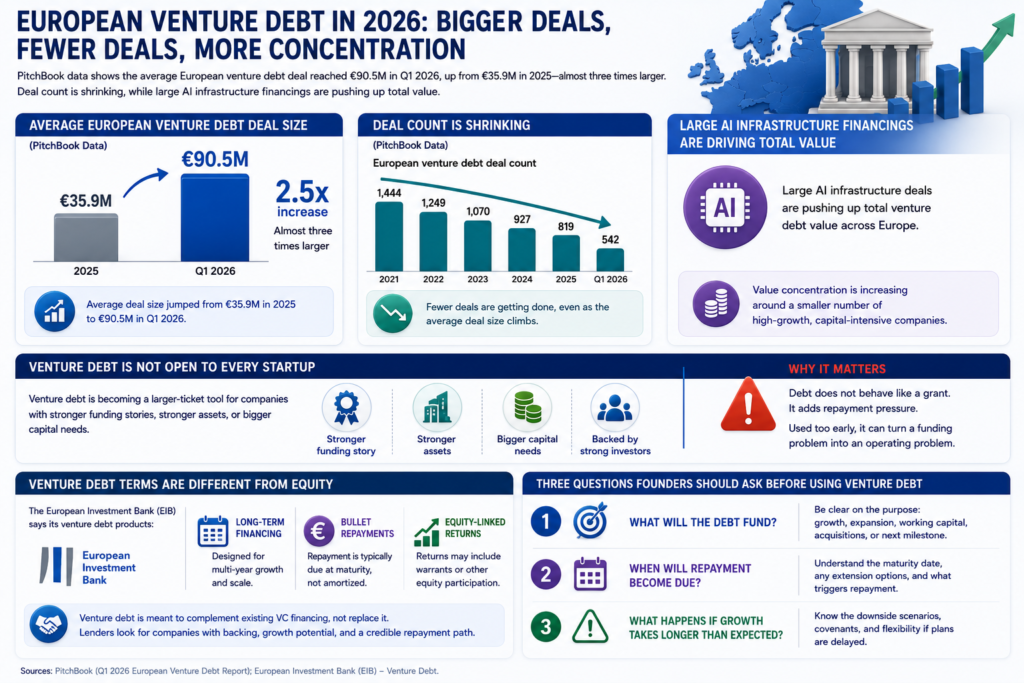

Venture debt is getting larger, not easier

European venture debt in 2026 also shows concentration. PitchBook reported that the average European venture debt deal reached €90.5 million in Q1 2026, up from €35.9 million in 2025. That is almost three times larger. The same report said deal count is shrinking, while large AI infrastructure financings are pushing up total value. This proves that venture debt is not suddenly open to every startup. It is becoming a larger-ticket tool for companies with stronger funding stories, stronger assets, or bigger capital needs.

This matters because debt does not behave like a grant. It adds repayment pressure. A founder should consider it only when the company has contracts, revenue, strong investors, working capital needs, or a clear next round. Otherwise, debt can turn a funding problem into an operating problem.

The debt structure also changes the founder’s risk

Venture debt terms matter because the structure is different from equity. The European Investment Bank says its venture debt includes long-term financing, bullet repayments, and equity-linked returns, and is meant to complement existing VC financing. That detail is important for founders. It means the lender is not only looking at the idea. They also want a company that already has backing, growth potential, and a credible repayment path.

Founders should ask three questions before using this route: what will the debt fund, when will repayment become due, and what happens if growth takes longer than expected?

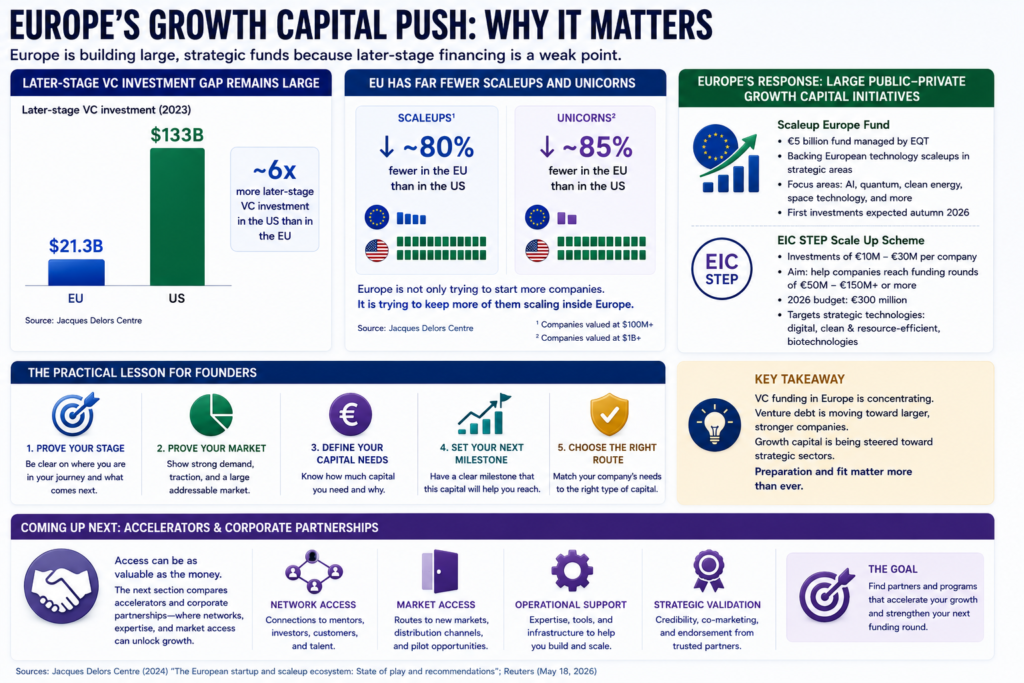

Growth capital is being pushed toward strategic sectors

Growth capital in Europe is also becoming more strategic. Reuters reported on May 18, 2026, that the EU selected EQT to run the €5 billion Scaleup Europe Fund, aimed at technology companies in areas such as AI, quantum computing, clean energy, and space technology. First investments are expected in autumn 2026. This is not a general startup fund for every early-stage business. It is a scaleup tool for companies working in sectors Europe sees as strategically important.

The EIC STEP Scale Up scheme shows the same direction from another angle. It offers investments of €10 million to €30 million per company, with the aim of helping companies reach funding rounds of €50 million to €150 million or more. Its 2026 budget is €300 million, and it targets strategic technologies such as digital technologies, clean and resource-efficient technologies, and biotechnologies.

Europe’s scaleup gap explains why these funds exist

Europe’s growth capital push exists because later-stage financing remains a weak point. The Jacques Delors Centre notes that EU later-stage VC investment was about $21.3 billion, compared with around $133 billion in the US. It also states that Europe has around 80% fewer scaleups and 85% fewer unicorns than the US. This helps explain why large public-private funds are being created. Europe is not only trying to start more companies. It is trying to keep more of them scaling inside Europe.

For founders, the practical lesson is clear. VC funding in Europe is concentrating. Venture debt is moving toward larger, stronger companies. Growth capital is being steered toward strategic sectors. Before choosing any of these routes, a startup should prove its stage, market, capital needs, and next milestone. The next section should compare this with accelerators and corporate partnerships, where access can be as valuable as the money itself.

Accelerators and corporate partnerships can unlock European market access

Accelerators and corporate partnerships in Europe can help founders get something capital alone cannot provide: faster access to mentors, buyers, technical partners, and investor networks. This matters in 2026 because many startups are not failing from a lack of ideas. They are struggling to prove demand, reach the right customers, or turn early interest into commercial use.

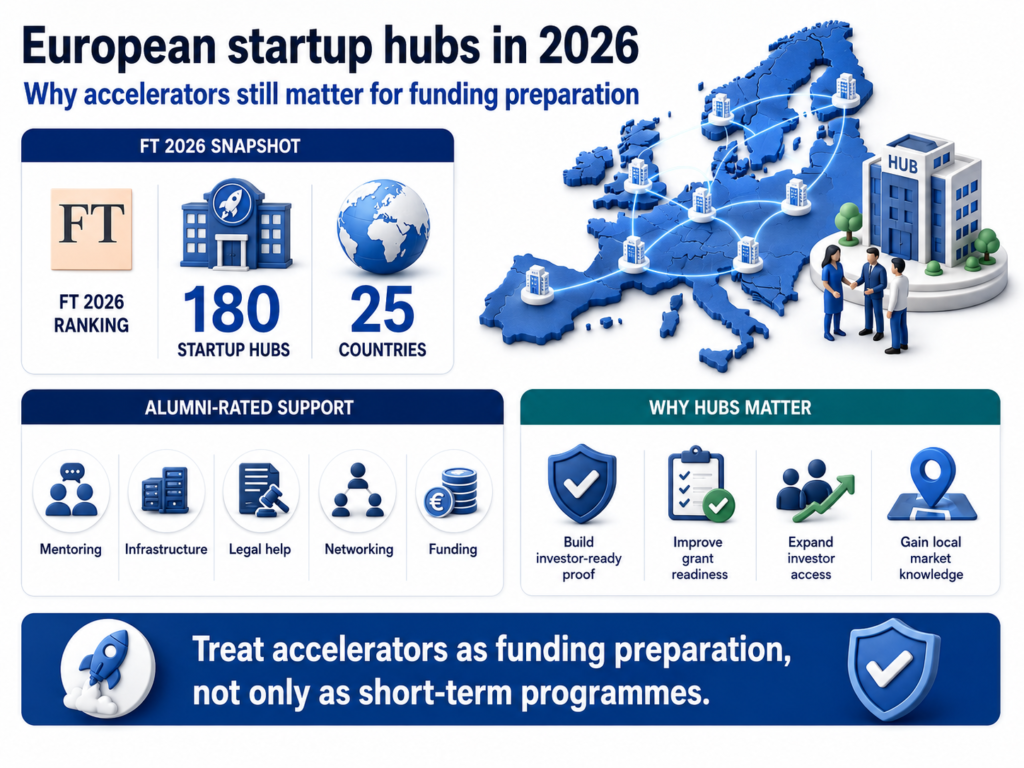

Startup hubs still matter for funding readiness

European startup hubs remain important because they help founders build the proof that investors and grant bodies expect. The Financial Times 2026 ranking covered 180 startup hubs across 25 European countries, with alumni rating support areas such as mentoring, infrastructure, legal help, networking, and funding. That shows why founders should treat accelerators as part of funding preparation, especially when the team lacks investor access or local market knowledge.

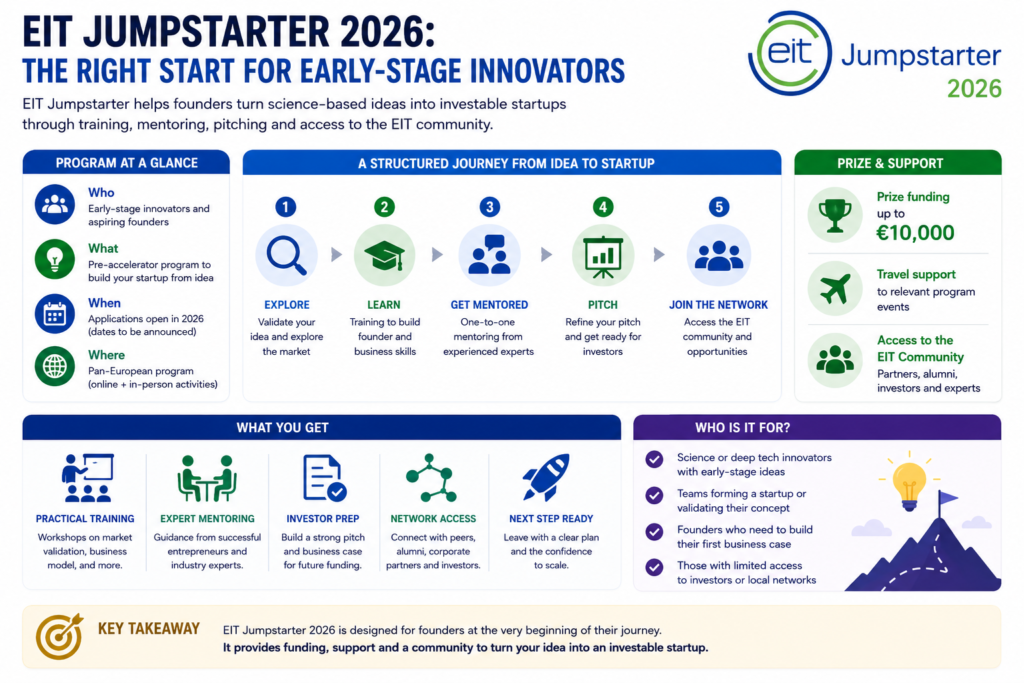

Pre-accelerators fit very early teams

European pre-accelerators can fit founders who still need to shape the business before raising serious capital. EIT Jumpstarter 2026 supports early-stage innovators with a structured journey from science-based idea to startup, including training, mentoring, pitching, and access to the EIT community. It’s a public materials list prize funding of up to €10,000, plus travel support, which makes it useful for founders still building their first business case.

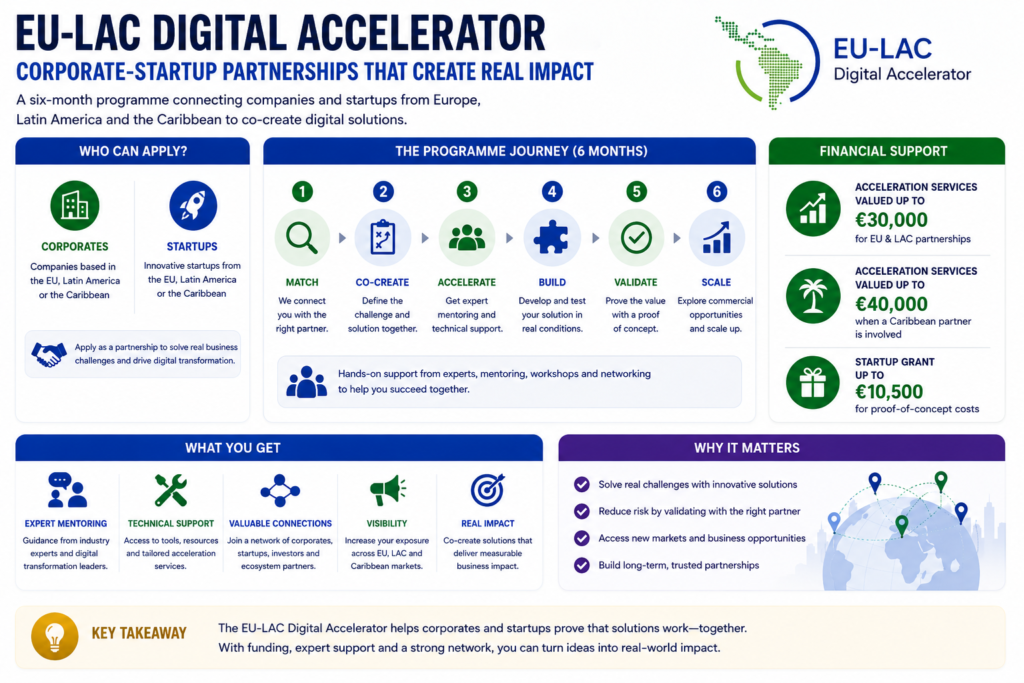

Corporate programmes can test commercial value

Corporate partnership programmes can help startups prove that larger organisations care about the solution. The EU-LAC Digital Accelerator, for example, runs a six-month programme for EU, Latin American, and Caribbean corporate-startup partnerships. It offers acceleration services valued up to €30,000, or €40,000 if a Caribbean partner is involved, plus startup grants of up to €10,500 for proof-of-concept costs.

Partnerships should support the funding story

Founders should choose accelerators and corporate programmes carefully. A strong programme should support one clear goal: customer access, pilot validation, technical support, market entry, or investor readiness. The EIC Business Acceleration Services also shows this direction, with support for corporate partnerships, global expansion, and investor access for EIC-backed companies.

For founders, the practical point is simple. An accelerator should create evidence that strengthens the next funding step. If it produces no pilot, customer signal, partner proof, or investor access, it can become a distraction. The next section should explain how founders can choose the right funding route before spending months on applications, pitches, or programmes.

Choose the funding route before building the application

European startup funding decisions should start with the work that needs capital, not the most visible fund name. A founder should first define the next milestone, then choose the route that can finance it with the least mismatch. If the company needs research, testing, or technical validation, grants, R&D programmes, or accelerators can fit. If the company has early demand but needs guidance and first outside capital, angels can make more sense. If the startup has traction, a large market, and a clear scaling path, VC becomes more realistic.

This order helps founders avoid weak applications and poor investor conversations. It also protects the business from accepting money that brings the wrong pressure. A grant can slow progress if the project scope is wrong. VC can hurt focus if the company is not ready for scale. Debt can create stress when revenue is still uncertain. The right source should support the next proof point, not force the startup into a funding story it cannot defend.

What founders should prepare before applying or pitching

European startup funding applications in 2026 need evidence that matches the funding route. The EIC reported 61 startups and SMEs selected in its latest Accelerator round, with €467 million in proposed funding and 85% receiving blended finance, so founders should expect deep checks on innovation, market readiness, and investment logic.

Eurostars shows how specific this can get: its March 2026 call offered up to €360,000 per project, covering up to 60% of costs for SME-led collaborative R&D.

| Funding route | Evidence to prepare |

|---|---|

| Grants | Project scope, budget, impact, delivery plan |

| Angels | Founder story, demand proof, first milestone |

| VC | Traction, market size, growth model |

| Crowdfunding | Audience proof, campaign page, risk notes |

| Debt | Cashflow, repayment plan, contracts |

Before writing anything, founders should decide which evidence proves the next milestone. This preparation stops teams from sending the same material everywhere. A grant reviewer needs project fit. An investor needs scale logic. A lender needs repayment confidence. Crowdfunding backers need trust, updates, and a reason to act early. This also makes weak gaps easier to fix before outreach begins properly.

How aboveA Helps Startups Prepare For Funding

Startup funding support in Europe should help founders choose the right route before they spend months applying or pitching. aboveA helps startups review their stage, market, proof level, and capital need so the funding path matches the business case. This matters because a startup looking for grant money needs different evidence than a team preparing for angels, VC, crowdfunding, or venture debt.

Our work focuses on the parts that funders actually check: market clarity, customer demand, go-to-market logic, use of funds, financial planning, and credibility signals. We also help founders turn scattered ideas into a clear funding story that explains why the business deserves attention now.

For European startups, this can reduce wasted time, weak applications, and unclear investor conversations. A stronger funding plan gives founders a better chance to approach the right source with the right proof.

Conclusion: Startup funding sources in Europe in 2026

Startup funding sources in Europe in 2026 give founders many options, but the strongest route depends on stage, evidence, and growth plans. Grants, angels, VC, crowdfunding, debt, accelerators, and growth capital all ask for different proof. Founders who match funding to a clear milestone will avoid weaker applications and poor investor conversations. The goal is not to chase every source. The goal is to choose the route that supports the next real business step with confidence and discipline in practice.

Grow Your Startup with Us!

aboveA Startup Incubator

Turn ideas into real businesses. aboveA Startup Incubator equips founders with practical tools, mentorship, and structured guidance to develop, validate, and launch their startups with confidence. Learn to scale, avoid common mistakes, and access resources designed for real-world success.

Startup Fundraising Readiness Services

Our startup fundraising readiness services can turn scattered traction, unclear positioning, weak credibility, and early market signals into a clearer investment case. We help startups prepare the proof, story, visibility, and go-to-market logic needed before serious investor conversations begin.

aboveA Product Launch / Market Entry Program

Launch with impact. Let us guide your startups through every step of introducing a product to new markets. From market research and validation to marketing strategies and operational readiness, founders gain the knowledge and support needed for a successful international market entry.

FAQ: Startup funding sources in Europe in 2026

Startup funding sources in Europe in 2026 raise practical questions about grants, investors, crowdfunding, debt, and funding-route fit for founders.

What are the main startup funding sources in Europe in 2026?

The main sources include grants, angel investors, VC, crowdfunding, accelerators, public loans, venture debt, corporate programmes, and growth capital for stronger scaleups with clear proof.

Which funding source is best for early-stage European startups?

Early-stage startups often fit grants, accelerators, angels, or crowdfunding when they can show customer learning, clear demand, founder strength, and a useful next milestone clearly.

Is venture capital right for every startup in Europe?

VC funding fits startups with large markets, fast growth potential, strong margins, clear traction, and a team that can scale beyond one local market.

How can European startups get non-dilutive funding?

European startups can use grants, public programmes, innovation loans, R&D funding, and accelerators when the project has clear scope, delivery ability, and measurable outcomes.

When should a startup consider crowdfunding?

Crowdfunding works best when a startup already has audience trust, a simple product story, visible demand, and the ability to deliver after the campaign.