Faustas Norvaisa

A Growth & Product Expert with 9 years of experience in revenue diversification, international expansion, SEO, and digital marketing. Passionate about scaling businesses and building global brands, he empowers companies to thrive with his motto, "sharing is caring.

How Thai Brands Can Expand Into Europe?

- Last time updated: 24th of January, 2026

Thai brands expanding to Europe often make the same entry mistake: treating “get a distributor” as the strategy. In Europe, buyers do not reward enthusiasm. They reward proof, clarity, and low-risk adoption. That changes how you should enter, and it changes when a partner actually helps.

This article shows how Thai companies can expand into Europe without local offices or distributors by first sequencing the right decisions: trust signals, channel choice, and demand testing. If you are trying to answer “Can we sell into Europe?” or “Do we need a local partner?”, this will help you make the call with less risk.

Enter Europe with proof, not hop - work with aboveA.

Table of Contents

Thai Brands Expanding to Europe: How Trust Works Differently in Europe?

Thai brands expanding to Europe often notice the shift immediately: buyers move more slowly, ask sharper questions, and treat trust like a checklist rather than a feeling. In many SEA markets, relationships can open doors fast. In Europe, procurement and decision-makers usually protect downside first. Even if they like your product, they want to see that the risk is contained and the process is reliable.

That difference shows up in a few repeat patterns:

Proof beats potential. “We can” matters less than “we have,” supported by references, outcomes, repeat orders, or verified performance.

Process is part of the product. Clear terms, timelines, responsibilities, and response cadence signal operational maturity. Improvisation signals risk.

Consistency builds confidence. If specs, pricing logic, or messaging changes between calls, buyers assume execution will also change.

Risk transfer gets rejected. Vague warranty, unclear returns, or fuzzy accountability slows decisions and pushes buyers back to known suppliers.

Reputation travels through networks. One credible reference, standard, or recognized partner can remove weeks of hesitation; the lack of it adds friction.

This is why Europe’s entry is not “just find a distributor.” A distributor can’t compensate for unclear positioning, thin proof, or messy commercial clarity. The companies that win early make one thing easy: for a European buyer to say, “This feels low-risk to test.”

Why for Thai Brands “Having a Distributor” Is Not a Shortcut?

Thai brands expanding to Europe often assume a distributor will remove friction. In reality, a distributor is not a bridge. It is a bet – and the bet only pays off when demand already exists, or your offer is easy to sell with low support cost.

Here’s what usually happens when companies go distributor-first too early:

-

You get “interest,” not commitment. Many distributors will say yes to a call, then quietly prioritize products that already move.

-

They push for control before performance. Exclusivity is often requested as insurance, even when there is no proven sales plan behind it.

-

Your product becomes a line item. If you’re one of 40 brands, you won’t get real attention unless you create pull through proof and clarity.

-

Pricing and feedback get lost. You stop hearing real objections from buyers, which makes it harder to improve positioning and close deals later.

-

The market stays invisible to you. If deals stall, you cannot tell whether the issue is demand, trust, price, or distributor effort.

A strong distributor relationship can be a powerful scaling lever. But it works best after you have basic evidence: who buys, why they switch, what proof they need, and what offer structure converts. Without that, a distributor does not reduce risk; it simply moves the risk from “market unknown” to “partner dependency.”

The smart sequence is simple: validate demand and messaging first, then choose partners from a position of leverage, not hope.

Why “Having a Distributor” Is Not a Shortcut?

With that said, Thai brands looking to expand to the EU often get better results by selling directly first, especially when the offer still needs refinement. Direct selling works best when buyers can evaluate your product remotely, the category does not require local installation or constant service, and you can reduce perceived risk through clear documentation, consistent communication, and simple commercial terms.

It is also the fastest way to learn what European buyers actually care about, because you hear objections firsthand instead of through a middle layer. That learning protects you from signing the wrong partner too early, pricing yourself into a corner, or letting someone else control your narrative. Direct selling is not “anti-distributor.” It is a leverage step. Once you have proof of intent, pilots, or repeat conversations, partner talks become practical and measurable rather than based on optimism.

Next, we will address where founders misread demand in Europe and how to test it before making irreversible commitments.

Where Thai Business Owners Misjudge Demand in Europe?

At this stage, Thai brands expanding to Europe often misread politeness as purchase intent. European buyers can sound positive, ask for a catalog, and still have zero urgency. The mistake is treating “interest” like demand, then building a channel plan on top of it.

Here’s a simple way to separate soft signals from real buying signals:

| What looks like demand (but isn’t) | What usually means demand is real |

|---|---|

| “Interesting, send more info.” | “What are your lead times, terms, and evaluation steps?” |

| Long gaps, no next meeting booked | A scheduled pilot, sample request, or technical review |

| Praise without specifics | Questions about switching, risks, and internal approval |

| One friendly contact | Multiple stakeholders pulled in (procurement, ops, finance) |

| “We’ll come back later” | Clear timeline and success criteria for a test |

This matters because European buyers compare options aggressively, and loyalty is weaker than founders assume. A Google survey reported that 58% of buyers who made a B2B purchase in the prior six months also switched vendors in that same period. That means buyers are willing to change suppliers, but only when the new option feels safer, clearer, and easier to justify internally.

To close this gap, you don’t need a European office or a distributor first. You need a controlled way to test whether buyers will move from “nice” to “serious,” which is exactly what we’ll map in the next section.

How Thai Businesses can Test European Demand Before Committing Anything?

With that clarity in mind, Thai businesses expanding to Europe should treat the first phase as evidence gathering, not “market entry.” The goal is to learn whether European buyers will move from polite interest to measurable intent, without you opening an office or handing leverage to a distributor. This is about running controlled tests that produce a decision you can stand behind.

1. Narrow Europe Down and Make Feedback Comparable

Europe is not one market, and “we spoke to a few countries” usually creates noise, not insight. Pick one or two regions where your offer has the highest chance to land. Your choice can be driven by where your ideal customers are concentrated, where similar products are already purchased, and where the buying culture fits your motion. The reason for narrowing is simple: you want feedback that can be compared side by side. When you stay focused, you can spot patterns quickly, and patterns are what reduce risk.

In this step, your success metric is not “we had meetings.” It is whether conversations become more specific over time. If every discussion stays generic, you do not yet have a positioning angle that creates urgency. If buyers start asking similar questions repeatedly, you’re getting close to a real market signal because they are evaluating you through a consistent lens.

2. Run Buyer-Led Conversations and Convert Them Into a Pilot

After region focus, shift into buyer-led discovery. This means you are not pitching features. You are learning what European buyers need to feel safe testing you. The strongest conversations are the ones that reveal disqualifiers: what makes a new supplier unacceptable, what proof must exist before a trial, and what internal steps approval requires. You are also listening for switching logic. Europe has plenty of suppliers already. The question is not “do they like it,” but “what would make them replace what they have.”

When the signal is strong, move into a controlled pilot. A pilot is not a discount and it is not a vague “let’s try.” It is a structured evaluation with clear success criteria. It gives the buyer a reason to act without asking them to take a leap of faith. If pilots are hard to get, that is information. It usually means the trust stack is incomplete, the offer is not yet framed as low-risk, or the category requires a different channel.

With that clarity in mind, Thai businesses expanding to Europe should treat the first phase as evidence gathering, not “market entry.” The goal is to learn whether European buyers will move from polite interest to measurable intent, without you opening an office or handing leverage to a distributor. This is about running controlled tests that produce a decision you can stand behind.

The Hybrid Model That Works for Thai Businesses in Europe Without Losing Control?

With that groundwork in place, Thai businesses expanding to Europe often find that the best path is neither “all-direct” nor “all-distributor,” but a hybrid approach that keeps learning and control on your side while still unlocking local reach.

1. What Hybrid Actually Means for Thai Businesses (and What It Is Not)?

Thai businesses looking forward to Europe often assume they must choose one path: go fully direct or hand everything to a distributor. In practice, the safest route is often a hybrid model that keeps control on your side while still using local reach where it truly helps.

A hybrid model means you run a direct motion for visibility, pricing control, and buyer feedback, while selectively working with partners only in areas where they add real value. The key is that partners do not “own” your market. They become a measurable channel, not a dependency.

Hybrid is not “we sell direct sometimes and also have a distributor somewhere.” That creates channel conflict, pricing confusion, and unclear accountability. A strong hybrid model has rules: which segments you sell direct, where partners operate, how overlaps are handled, and how commercial terms stay consistent enough to protect trust.

In Europe, hybrid often works best when you face multiple regions or buyer types. You keep strategic accounts direct, use partners for coverage, and keep learning flowing.

2. How Thai Brands can Keep Partners Useful Without Becoming Dependent?

Thai brands expanding to Europe often think they must pick one lane: go fully direct or hand the market to a distributor. A hybrid model is safer because it keeps control with you while still using local reach where it truly helps.

In a hybrid setup, you keep a direct motion to hold pricing authority, capture buyer feedback, and maintain leverage in negotiations. Partners are added only where they bring real lift: local language, service coverage, or access to specific accounts, and they operate under clear rules so they don’t “own” the market.

| Model | Control | Learning speed | CAC impact |

|---|---|---|---|

| Direct only | High | Fast | Drops as proof grows |

| Partner only | Low | Slow | Can rise without proof |

| Hybrid | High–Medium | Fast | Stabilizes as reach grows |

This is where some Thai businesses work with aboveA to validate demand, sharpen positioning, and build repeatable buyer conversations first – so partner discussions happen from leverage, not guesswork. That keeps the entry reversible until the signal is strong, and prevents exclusivity from becoming a trap.

Thai Businesses Selling to EU: How to Build Buyer Confidence Faster?

European buyers rarely decide based on excitement. They decide when the purchase feels easy to justify internally and low-risk to test. That means “trust” is not a vibe. It is a set of assets you can show.

The first asset is credible proof. Not broad claims, but specific evidence that your product performs in real conditions. This can be customer outcomes, repeat orders, performance comparisons, or documented results. Proof matters because it reduces the buyer’s personal risk. They don’t want to be the person who chose the unknown vendor without backup.

The second asset is commercial clarity. Buyers move faster when pricing logic is consistent, responsibilities are clear, and terms don’t feel improvised. If a buyer senses negotiation chaos, they assume delivery and support will be chaotic too. Clean structure reads as operational maturity.

The third asset is reliability signals. Response time, follow-up cadence, the ability to answer hard questions without delays, and consistency across documents all signal that you will not create downstream problems. This is often more persuasive than flashy branding.

This is where some Thai companies use aboveA in a practical way: to translate what European buyers expect into a proof-first story, tighten the offer so it feels low-risk to test, and structure conversations so momentum doesn’t die after the first “sounds interesting.”

Next, we’ll cover when partner-led entry becomes the right move, and how to choose partners without losing control or margin.

When Partner-Led Entry Becomes the Right Move for thai Businesses?

If you are a Thai company wanting to enter Europe, first, you should treat partner-led entry as a tool, not a default. It works best when a local player removes friction you cannot solve remotely, local language, dense industry relationships, on-site service or installation, or support expectations buyers won’t waive. In those cases, the partner doesn’t just “sell for you.” They make the purchase feel safer inside the buyer’s organization.

The common mistake is choosing partners for comfort, not performance. A distributor saying “we can handle Europe” is not a plan. A plan includes target accounts, the positioning angle they will use, and proof they can create pipeline rather than simply list your product.

A quick check is whether the partner agrees to measurable activity and transparent reporting from day one. If they avoid visibility, push for exclusivity early, or can’t explain how they will generate demand, you risk losing time and control.

Next, we’ll cover the red flags that signal a bad distributor deal before you sign anything.

Red Flags Thai Exporters should consider as a Bad Distributor Deal

Thai exporters expanding to Europe should learn to spot bad distributor deals early, before they become expensive distractions.

The first red flag is exclusivity before evidence. If a distributor wants exclusive rights while you still lack demand proof, you are trading leverage for hope. The second is no concrete go-to-market plan. “We have customers” is not a plan; you need target segments, priority accounts, and a clear outreach approach. Third is low visibility. If you cannot see what accounts are being worked, what feedback is coming back, or why deals stall, you lose learning and control. Fourth is pricing chaos. If the distributor sets pricing without shared logic, your brand can be positioned inconsistently, which damages trust fast in Europe. Fifth is unclear responsibilities. If support, warranty, returns, and delivery ownership are vague, problems turn into blame games and buyers feel the risk.

Next, we’ll tie everything together with a simple framework to choose direct, partner-led, or hybrid entry.

How to Choose Direct, Partner-Led, or Hybrid Entry as Thai Businesses?

With those red flags clear, Thai businesses expanding to Europe can stop debating “direct vs distributor” as a gut feeling and start treating it like a decision you can justify. The right choice depends on category friction, how buyers validate trust, and how much control you need while you learn. The table below helps you pick a path quickly, then pressure-test it with reality.

Use this table to make the call fast:

| Decision question | If “Yes” → best path | Why it fits |

|---|---|---|

| Can buyers evaluate and approve your product without local presence? | Direct first | You keep control, learn fast, and build proof without dependency. |

| Does the category require local service, installation, or heavy relationship access? | Partner-led | A local partner removes friction you cannot solve remotely. |

| Do you want coverage across regions but still need visibility and pricing control? | Hybrid | You scale reach while keeping feedback loops and leverage. |

| Is your positioning/pricing still evolving? | Direct first | Partners lock assumptions too early and slow iteration. |

| Do deals stall because buyers need local reassurance more than product proof? | Partner-led or Hybrid | Local presence reduces perceived risk and speeds internal approval. |

Once you pick a path, align it to your proof level. If you don’t yet have repeatable evidence (pilot requests, procurement involvement, clear timelines), starting partner-first usually increases dependency and hides the real objections. If you do have signal, partners become a scale lever rather than a rescue plan.

Next, we’ll close with how to structure your first Europe test so it creates proof you can reuse, no matter which entry path you choose.

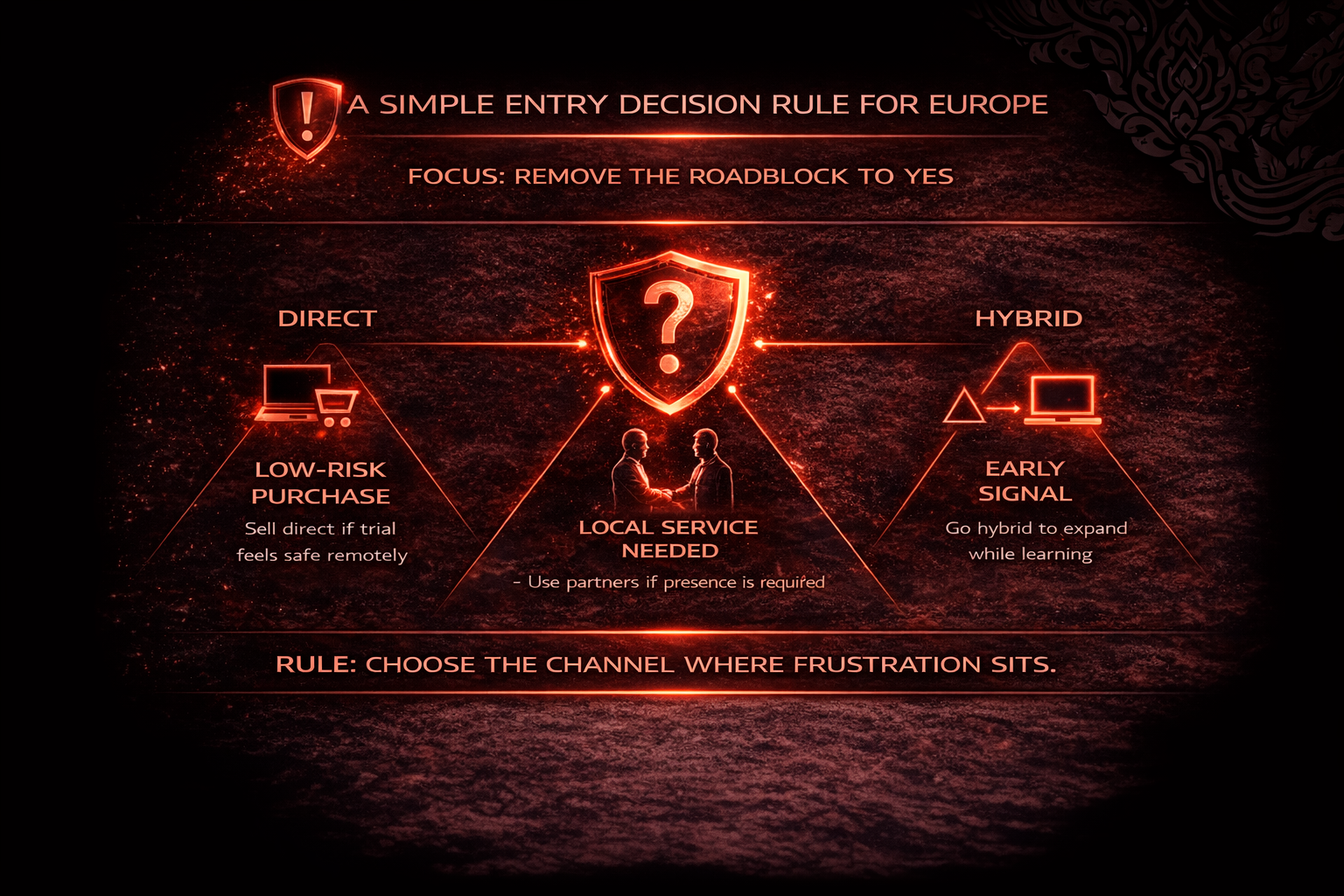

A Simple Entry Decision Rule for Thai Brands Targeting Europe

With the channel options clear, Thai brands that want to penetrate the European market should make the decision based on one thing: where trust friction sits. If buyers can evaluate your offer remotely and the purchase feels low-risk to trial, start direct. Direct selling keeps feedback clean, protects pricing logic, and helps you learn what Europeans actually need to see before they commit.

If deals stall because the category demands local service, installation, language coverage, or relationship access you cannot replicate remotely, partner-led entry becomes practical. In that case, the partner’s job is not “distribution.” It is risk reduction inside the buyer’s organization.

Hybrid is what you use once early signal exists. It keeps strategic accounts and learning loops direct, while adding partners for coverage without losing visibility. The mistake is choosing a model based on comfort. Choose it based on what blocks the buyer from saying yes, then evolve the model as proof grows.

Thai Brands Expanding to EU: Conclusion

Thai brands expanding to the EU win by sequencing decisions before commitments. Start by testing demand in one focused region, then build proof that makes buyers feel safe to trial. If evaluation can happen remotely, go directly to learn fast and keep pricing control. If local service, language, or relationship access is required, use partners with clear accountability. Once the signal is repeatable, shift to a hybrid model that scales reach without losing visibility and keeps entry reversible until Europe confirms traction.

Thai Business Expansion into the EU: Frequently Asked Questions

Can Thai brands expanding to EU sell without a local office?

Yes. Many Thai brands sell into the EU remotely by focusing on proof, clear terms, and a low-risk pilot. Build trust first, then scale the channel that converts.

Do we need a distributor to enter the EU?

Not always. Distributors help when local service, language, or access is truly required, but they’re not a shortcut. Validate demand first so you don’t trade leverage for exclusivity.

How can aboveA help Thai businesses expand to the EU without overcommitting?

aboveA helps you validate demand, sharpen positioning, and structure buyer conversations so you get a real signal (pilots, timelines, procurement involvement) before you commit to partners or setups.

What do European buyers need to trust a new Thai supplier?

They want risk reduction: credible proof, consistent documentation, predictable follow-up, and clean commercial clarity. aboveA often helps package this into a proof-first story that buyers can justify internally.

When should we move from direct selling to a hybrid model in Europe?

When intent becomes repeatable: pilot requests, multiple stakeholders, or clear timelines. Hybrid keeps strategic accounts direct for learning while using partners for coverage with rules and reporting.